Frances serves a sophisticated and international clientele, with contacts in the US, Europe, Australia, Asia, and the Middle East. This helps maximize demand for her clients, especially given the increasingly global bid for New York City real estate.

Frances possesses a sharp and detailed memory for real estate data, such as apartment layouts, building histories, existing and pending new developments, resale comparables, pricing, and the historical financial performance of neighborhoods, buildings and apartments.

This knowledge, along with a deep rolodex and an appreciation for her clients desire for premium service, discretion, and efficiency, has earned Frances the loyalties of financiers, celebrities, real estate investors, developers, and the art culture of New York City.

In addition, buyers and sellers alike benefit from her honest and straight forward approach to real estate, investment analysis, and her creative financial consultation.

Frances serves a sophisticated and international clientele, with contacts in the US, Europe, Australia, Asia, and the Middle East. This helps maximize demand for her clients, especially given the increasingly global bid for New York City real estate.

Frances possesses a sharp and detailed memory for real estate data, such as apartment layouts, building histories, existing and pending new developments, resale comparables, pricing, and the historical financial performance of neighborhoods, buildings and apartments.

This knowledge, along with a deep rolodex and an appreciation for her clients desire for premium service, discretion, and efficiency, has earned Frances the loyalties of financiers, celebrities, real estate investors, developers, and the art culture of New York City.

In addition, buyers and sellers alike benefit from her honest and straight forward approach to real estate, investment analysis, and her creative financial consultation.

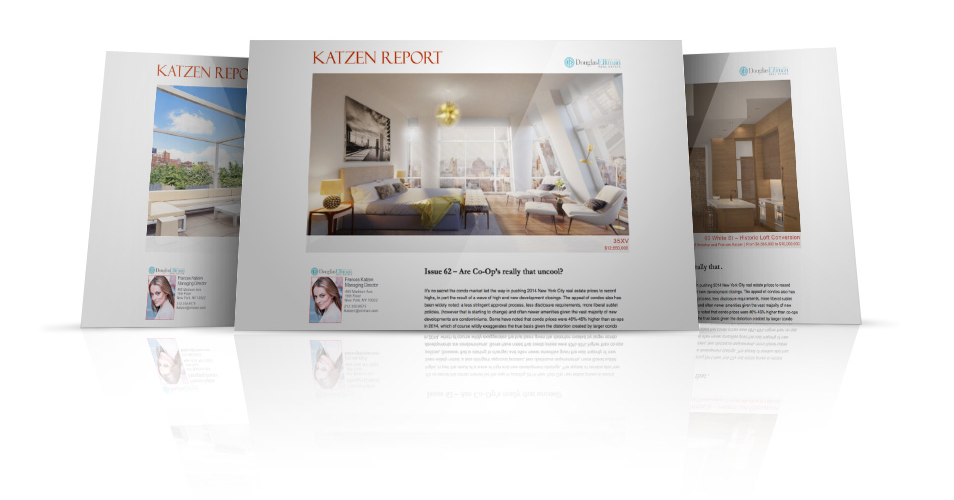

PROVIDING CRUCIAL UP-TO-THE-MINUTE REAL ESTATE DATA – WITH A PULSE ON THE NYC PROPERTY MARKET. THIS IS YOUR REAL ESTATE RESOURCE, PROVIDING MARKET INSIGHTS NOT AVAILABLE ANYWHERE ELSE.

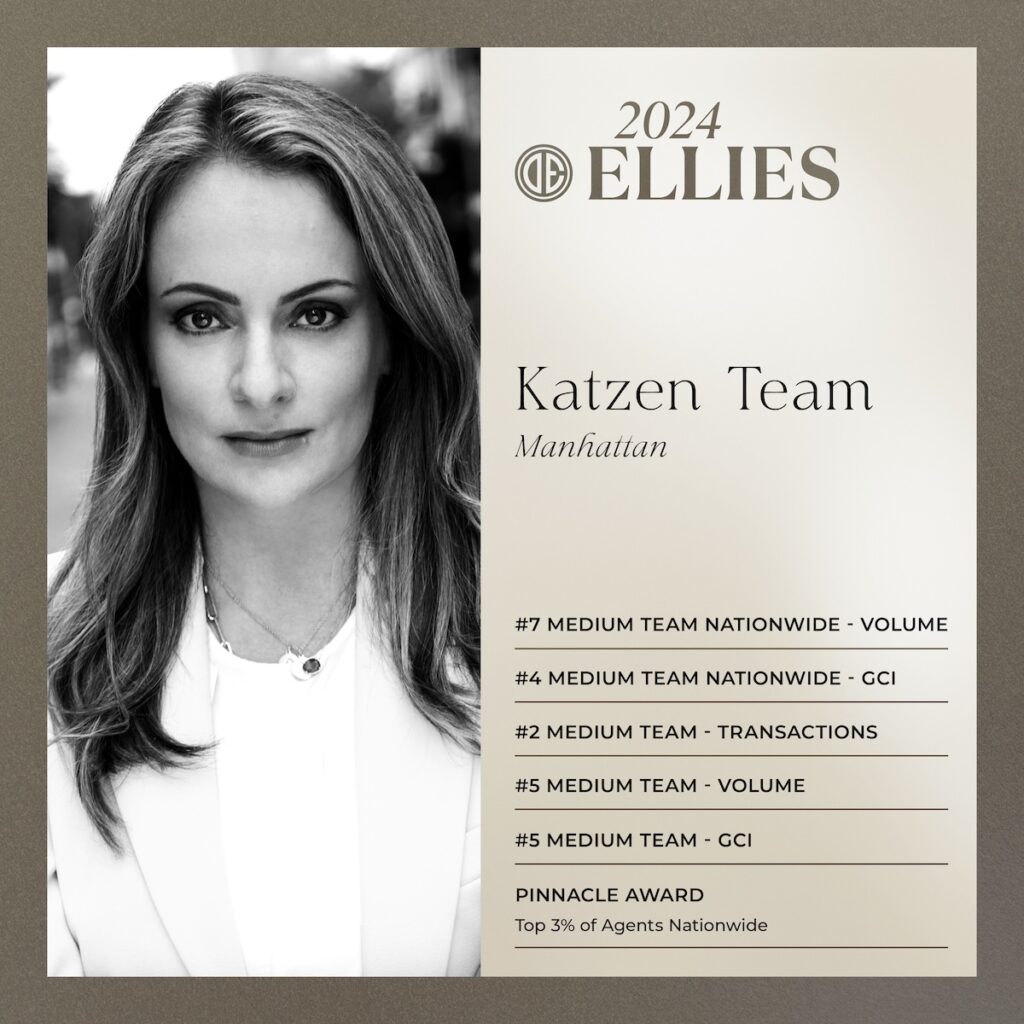

is proud to have received the following Douglas Elliman “Ellies” Awards for 2024!

#4 Top Achievements in GCI – Medium Teams – Manhattan

#5 Top Achievements in Volume – Medium Teams – Manhattan

#2 Transactions – Medium Teams – Manhattan

#4 Medium Team Nationwide GCI

#7 Volume Pinnacle Award – Medium Teams – Nationwide

THE KATZEN TEAM

is proud to have received the following Douglas Elliman “Ellies” Awards for 2024!

#4 Top Achievements in GCI – Medium Teams – Manhattan

#5 Top Achievements in Volume – Medium Teams – Manhattan

#2 Transactions – Medium Teams – Manhattan

#4 Medium Team Nationwide GCI

#7 Volume Pinnacle Award – Medium Teams – Nationwide

Testimonials

"Working with Frances was an absolute game changer—she found my family a stunning off-market gem we never would have discovered on our own. Her deep connections and relentless hustle uncovered a space that perfectly matched our vision and budget. She also navigated a tumultuous negotiation process with pure excellence. In a city as competitive as New York, her ability to deliver rare opportunities is nothing short of extraordinary."

Pierre & Sandy DebbasPartner of Romer Debbas, LLP

"When I was looking for a realtor in New York I wasn't sure where to start. A friend told me about Frances, actually. I think she's an excellent real estate agent who will be sure to get you the best price."

JACQUELINE PATA

"Frances Katzen provides a ton of value and has an abundance of knowledge about the real estate market here in New York Cityl"

Dan Herzog

I want to thank you for a job very well done. You were terrific in marketing and selling our loft and in managing the buyer through the closing process. As someone involved in new condo development in Manhattan it was a pleasure to see how well you understood the market and the marketing process as well as the closing process. I would highly recommend you to anyone looking for a top-tier team to sell their apartment.

Anthony V. LabozzettaPresident of Madison Equities, LLC

"Frances Katzen is extremely knowledgeable and professional. Highly recommend her!"

ASHLEY harris

Selling a property while living across the county

is a challenging and scary position to be in. You

have to have complete faith in a team that can

successfully manage the relationships needed to

sell a home.The contractors, the building

management, the lawyers, the stagers…

I feel fortunate to have found and worked with

Frances Katzen and her team.

They made it easy, efficient, and seamless.

My place sold within days of being on the

market. With my approval, Fran and her team

managed the conversations with all the relevant

stakeholders on my behalf to get the home sold

for the maximum price.

Ongoing communication was excellent, and they

took the worry and hassle away from me.

This has been honestly the best real estate

transaction I have ever been a part of.

Lynn & Alex Flynt

Fran Katzen is the lady to go to when seeking discretion, great negotiation, honest dealings –value of my time, and efficiency. She was to the point and I consider her a friend as well as my broker.

MICHAEL STRAHANNY GIANT DEFENSIVE END

"Frances, we just wanted to send a separate thank you to you. I know at times this was very hard for us given the circumstances, but we are very appreciative of all the work you and your team put in to selling our apartment. It was hard being on the other side of the country through a pandemic and while it was all happening, but we really felt lucky to work with you. Thank you for such a stellar job!"

Laura & Michael Constantiner

Buying in NYC is so much different than buying in San Francisco. The Katzen Team, represented by Lancelot Watson-Taffe, made the experience much less stressful. His client-focused service, hard work and his ability to plan ahead is second to none. Fran Katzen is the ultimate relator with a deep knowledge of the market and negotiation. As a seasoned banker, it is hard to impress me (lol) but I am indeed impressed!!

Margaret MakExecutive Director First Republic Bank

"First of all, congratulations on an excellent job shepherding our transaction through the choppy waters we encountered. But for your expert advice and counsel, the outcome might have been different. Well done."

Roger & Lou Keating

Frances Katzen and her team were amazingly helpful and efficient throughout the entire process of searching for, and closing on, my apartment in New York City. They were extremely diligent and very available to provide answers to questions and give advice on the negotiation process and the many other moving pieces of a Manhattan real estate deal. I am so thankful that I chose to work with them and they would absolutely be my only choice for any future real estate needs.

Conor DevineGUGGENHEIM PARTNERS

"The lovely Frances Katzen is a delightful, 5-star real estate guru, known for her knowledge of NYC luxury markets, strikingly able to bring out the most desirable features of a property, no matter the price level. She’s a virtual magician in directing attention to its functionality and what yet may be done. Could not have gotten this closed in this insane climate without her!"

Diana Brian

I want to express my extreme satisfaction with Fran, Lance and the rest of the Katzen Team

Over the last 6 years Fran has helped me sell three condominiums in Manhattan. Most recently our collaboration included the sale of an apartment in Midtown. Despite the difficult market conditions, Fran and her team helped develop a selling strategy that reimagined the apartments space and look...a necessity in this environment.

I chose Fran because of her professionalism and insight. I'm so glad I did as the property went to contract soon after listing.

Ronald Goldstein

The selling of an apartment and especially co-op apartments in New York City can be a difficult undertaking. And at times, as the process grinds on, it can become arduous. This and more occurred on a recent transaction. I am writing to document the fact that if it wasn’t for Frances Katzen, I do not believe this transaction would have closed.

It was thanks to her professionalism, composure, knowledge and resolution based thinking that the sale eventually occurred. If given the opportunity to sell another NYC apartment, I would only utilize her services and would therefore unequivocally recommend her to others.

Gavin TollmanCEO at Trafalgar Tours

There is only one Michael Jordan of the real estate market and it’s spelled: F-R-A-N!!!

Sally & Shane Tienmman

Fran, thank you! It was such a pleasure working with you. I can’t even describe how great an experience it was having you as our realtor. Definitely above and beyond any of our past experiences. Thank-you!!!

Mariano Guzman

I am writing this to express my extreme satisfaction with Fran, Lance and the rest of the Douglas Elliman Katzen Team

Over the last 6 years Fran has helped me sell three condominiums in Manhattan. Most recently our collaboration included the sale of an apartment in Midtown. Despite the difficult market conditions, Fran and her team helped develop a selling strategy that reimagined the apartments space and look...a necessity in this environment.

I chose Fran because of her professionalism and insight. I'm so glad I did as the property went to contract soon after listing.

I very much recommend her Team !

Ronald Goldstein

We just received an email from Stu and the close is done!

We just wanted to thank you for your help, professionalism, your outstanding way to answer so promptly all our questions.

It's has been a real pleasure to work with you and I am sure we will work again very soon all together on our next project.

Emmanuel Geindreau-Banchik & Steven Banchik

My wife and I had a wonderful experience working with Frances Katzen and her team. The attention to detail, constant feedback on showings, market guidance and personal attention made me feel like I was their only client. I would highly recommend using the Katzen team on your next listing in New York if you want a really positive experience with results!

Jack McKillip

Fran, It has been an absolute pleasure working with you. This is not always the easiest process, but to be able to smile and laugh with you thru all of the craziness makes it all the more enjoyable and is much appreciated. This home is just beautiful. Thank you for all that you do.

Sally & Shane T.

“Frances congratulations on selling my home in New York. It was smooth and wonderful; your company is great. Thank you so much. Hope to see you again.”

Pat Cooper

I wanted to thank you for all your efforts on 1st Street and seeing the project through. You did a great job with little to work with in the early days and I wanted to make sure you know I, and my partners, are appreciative of all your efforts and I personally want to thank you and congratulate you on a job well done.

I hope to work with you again,

Eckstein Development

As a real estate developer, I interact with numerous brokers in several marketplaces. Having worked with Fran Katzen on both the buy and sell side, I can confidently say that she is among the best brokers in the country. While working with Fran when my wife and I were looking for a home, she explained everything very clearly and had a strong understanding of all of the technical points. Frances’s negotiations were strong, and she is certainly a deal maker with a knack for getting it done. I have referred Fran to several of my close friends and family members and would strongly recommend her to anyone who is looking for a hardworking, honest and highly skilled broker.

NEIL GEHANIPRESIDENT OF TRILOGY REAL ESTATE GROUP

I had Frances and her team represent my home. Frances and her team worked extremely proficiently, accurately, and with tremendous focus. She was able to fetch, what I believe, one of the highest prices in the building. Considering the current state of the market… As you can imagine I was very pleased with the results. I am happy to endorse Frances and her team to any owner who is seeking to list their apt.

PETER HESSHESS ARCHITECTS AND DESIGN TEAM

When my wife and I set upon the process of looking for an apartment in New York City, we were uneducated in the dynamics of that marketplace. Fortunately for us, we met Fran Katzen in the early stages of our search. Fran took the time to fully understand what we were looking for, patiently showed us an appropriate variety of apartments, and then was highly effective and efficient as we zeroed in and closed on the property we decided upon. Fran was a pleasure to work with throughout. Her level of professionalism and knowledge of the New York market is second to none. The energy that she devoted to us as a client seemed endless. Fran was also extremely effective in representing us during negotiations on price and important closing details. It is without hesitation that I recommend Fran.

THOMAS W.SENIOR VP, GLOBAL HEAD OF EQUITY TRADING, SANFORD C. BERNSTEIN & CO., LLC

It is with great pleasure that I write this letter on behalf of Frances Katzen. In May of this year I interviewed several real estate brokers to sell my apartment in Manhattan. Every realtor who wanted my business recommended I put my apartment on the market at an unrealistic asking price. Ms. Katzen came prepared with comparable listings and recent sales and educated me about the current market. We agreed upon a realistic listing price and ultimately sold and closed on the apartment in under three months at full asking price. With other realtors the property would easily have been on the market for many more months with reductions to the asking price. Ms. Katzen has a passion for her work. She and her staff are dedicated professionals who were available to me at a moment’s notice. Ms. Katzen even negotiated our deal while she was traveling overseas. I was able to reach her during this crucial period as if she was working down the block. In a difficult real estate market I could not have been more satisfied with Frances’ work. Her tireless energy, savvy business skills, relentless marketing and frequent showing of the apartment were the reason for the expeditious sale at asking price, unheard of in this market. Not only do I recommend Frances, I would listen to her carefully and take her advice regarding sales strategies.

ANDREW B.ATTORNEY OF LAW

I was so impressed with Frances when she helped me with the purchase of a new apartment, that I also had her help with the sale of the old one. I trust Fran’s advices explicitly because she has the ability to know what I wanted to accomplish.

NANCY CHONG KONG

Fran did a truly outstanding job selling our apartment. She exceeded our expectations in several ways….from her initial marketing of the unit, to how she handled several negotiations with interested parties to achieve the highest price, to how she worked with the buyer post-signing to navigate a very choppy NYC mortgage environment. Despite listing our apartment at a challenging time for NYC real estate, Fran achieved a great result and followed through to closing. I will be recommending Fran to any of our friends who are looking for a broker.

MICHAEL C. PRINCIPALPRIVATE EQUITY PROFESSIONAL

“Out of the huge universe of brokers, it’s rare that you find someone who truly hand-holds you through the process and works tirelessly on your behalf. Frances Katzen is that type of broker, and has a work ethic which I believe is unmatched. She has an innate sense for this sometimes challenging market and has time and again sold ‘unsellable’ properties in ‘difficult’ markets at a premium to comps on offer. I always recommend Fran based on my several exceptional experiences in buying and selling real estate (through her) in New York.